Blockchain-powered real-time tax revolution

Taxation has long operated on a delayed cycle. Businesses and individuals file returns after the fact, and tax authorities audit or collect months later. This retrospective approach creates delays, compliance costs and room for evasion. Now, a new paradigm is emerging whereby embedding tax collection into transactions as they happen and this real-time model is gaining momentum. As global public debt climbs above $100 trillion, governments are under pressure to improve efficiency and digital trade and decentralised workforces further strain traditional systems. Meanwhile, programmable payment solutions such as stablecoins, API triggered bank payments and central bank digital currencies (CBDCs) are introducing programmable money, so opening the door to real-time, rule-based tax collection. In 2015, 73% of global tax experts expected blockchain to power tax systems by 2025 - today, that vision is materialising.

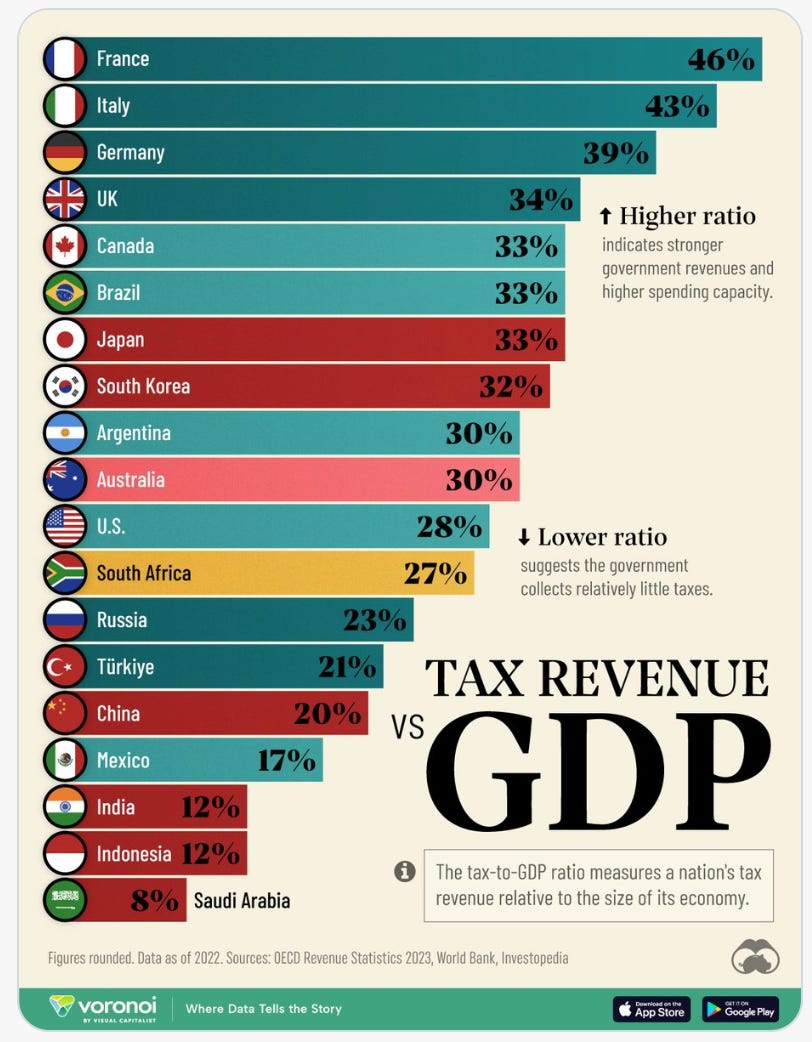

Source: Visual capital

Tax revenue is foundational to public services. In the U…